1 HealthView Services, “Medicare and Social Security COLAs: Putting the 2023 Numbers into Context,” October 2023.

2 The Nationwide Retirement Institute, “2022 Health Care Cost in Retirement Survey,” October 2022.

3 HealthView Services, “2022 Retirement Healthcare Costs Data Report,” March 2022.

4 Medicare. “Costs”. Accessed January 30, 2025.

5 Medicare. “Monthly premium for drug plans.” Accessed January 30, 2025.

6 U.S. Department of Health and Human Services, “How Much Care Will You Need?” 2020.

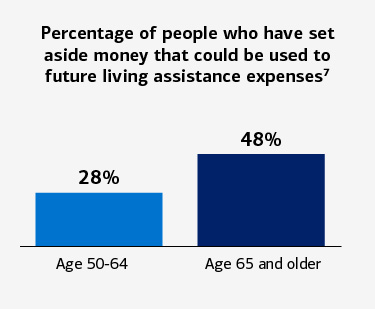

7 American Association for Long Term Care Insurance. 2022 long-term care insurance statistics data facts. Accessed January 30, 2024.

8 Kaiser Family Foundation. “The Affordability of Long-Term Care and Support Services: Findings from a KFF Survey.” November 2023.

9 Genworth, “Cost of Care Trends and Insights,” 2022.

10 You can receive tax-free distributions from your HSA to pay or be reimbursed for qualified medical expenses you incur after you establish the HSA. If you receive distributions for other reasons, the amount you withdraw will be subject to income tax and may be subject to an additional 20% tax, unless an exception applies. Any interest or earnings on the 411 assets in the account are tax-free. You may be able to claim a tax deduction for contributions you, or someone other than your employer, make to your HSA directly (not through payroll deductions). In addition, HSA contributions may reduce your state income taxes in certain states. Certain limits may apply to employees who are considered highly compensated key employees. Bank of America recommends you contact qualified tax or legal counsel before establishing an HSA.

This material should be regarded as educational information on healthcare considerations and is not intended to provide specific healthcare advice. If you have questions regarding your particular healthcare situation, please contact your healthcare, legal or tax advisor.

Long-term-care insurance coverage contains benefits, exclusions, limitations, eligibility requirements and specific terms and conditions under which the insurance coverage may be continued in force or discontinued. Not all insurance policies and types of coverage may be available in your state.

Life insurance policy guarantees are backed by the claims-paying ability of the issuing insurance company. They are not backed by Bank of America, Merrill or its affiliates, nor does Bank of America, Merrill or its affiliates make any representations or guarantees regarding the claims-paying ability of the issuing insurance company.

You can receive tax-free distributions from your HSA to pay or be reimbursed for qualified medical expenses you incur after you establish the HSA. If you receive distributions for other reasons, the amount you withdraw will be subject to income tax and may be subject to an additional 20% tax, unless an exception applies. Any interest or earnings on the 411 assets in the account are tax-free. You may be able to claim a tax deduction for contributions you, or someone other than your employer, make to your HSA directly (not through payroll deductions). In addition, HSA contributions may reduce your state income taxes in certain states. Certain limits may apply to employees who are considered highly compensated key employees. Bank of America recommends you contact qualified tax or legal counsel before establishing an HSA.

Merrill, its affiliates, and financial advisors do not provide legal, tax, or accounting advice. You should consult your legal and/or tax advisors before making any financial decisions.

This information should not be construed as investment advice and is subject to change. It is provided for informational purposes only and is not intended to be either a specific offer by Bank of America, Merrill or any affiliate to sell or provide, or a specific invitation for a consumer to apply for, any particular retail financial product or service that may be available